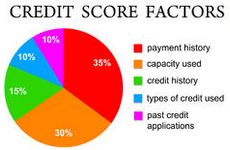

A credit score is a mathematical model used by a majority of banks to evaluate a person’s financial reliability or credit risk. The score gives lenders a “lend/reject” answer for people applying for credit or loans. A credit score is also commonly referred to as a FICO Score (Fair Isaac and Company), after the company that came up with the scoring method and software now used by banks, lenders, insurers, and other businesses today. Fair Isaac worked with each of the three major credit bureaus (Experian, Equifax, and TransUnion), to create a scoring method that takes into account the following factors:

A credit score is a mathematical model used by a majority of banks to evaluate a person’s financial reliability or credit risk. The score gives lenders a “lend/reject” answer for people applying for credit or loans. A credit score is also commonly referred to as a FICO Score (Fair Isaac and Company), after the company that came up with the scoring method and software now used by banks, lenders, insurers, and other businesses today. Fair Isaac worked with each of the three major credit bureaus (Experian, Equifax, and TransUnion), to create a scoring method that takes into account the following factors:

Payment History (35%)

This component inspects how well you meet your prior obligations on different account types. It also examines past problems such as bankruptcy, collections, and delinquency. It considers the severity of the problems, the time it took to resolve them, and how long it has been since the problems occurred. The more problems there are in your credit history, the weaker your credit score.

Amounts Owed (30%)

This category is the amount you currently owe to lenders, an indicator of your present financial situation. The focus is mainly on your current amount of debt, but it also considers the number of accounts and specific types of accounts that you hold.

Length of Credit History (15%)

This includes both the time since your accounts have been open, as well as the time it has been active. This category is pretty straightforward; the longer your history of making timely payments, the higher the score.

Types of Credit Used (10%)

Having various accounts, such as installment loans, mortgage, retail accounts, and credit cards may improve your score.

New Credit (10%)

Your score considers how many new accounts you have applied for recently and when you last opened a new account. It assumes people who apply for credit a lot have financial pressures, so each new credit lowers your score a little.

A person’s credit score ranges between 300 to 850. A score of about 690 or higher indicates a very good credit history, which definitely helps the person get approved for loans with better interest rates or credit cards with attractive perks. Those with scores below 630 will often find financing at a favorable rate significantly more difficult. A credit score evaluates both positive and negative information in your credit report; for example, late payments will lower your score, but establishing a good track record of making on-time payments will raise your score. Although a credit score is only calculated from the information in your credit report, when lenders are making a credit decision they may also look at other information, such as your income, how long you have worked at your current job, and what kind of credit you are requesting.